Starting a business in India has become significantly more streamlined over the years, thanks to regulatory reforms like the Companies Act 2013. Among the various types of companies, a Private Limited Company is one of the most popular and preferred structures for entrepreneurs due to its benefits such as limited liability, separate legal identity, and ease of operations. In this blog, we will discuss the process of incorporating a Private Limited Company under the Companies Act 2013, and provide insights into Private Limited Company Registration in India, Pvt Ltd Company Registration in India, and more.

What is a Private Limited Company?

A Private Limited Company (Pvt Ltd) is a business entity that is privately held, with the liability of its shareholders limited to the amount of capital they have invested in the company. The key features of a Private Limited Company include:

Limited Liability: Shareholders’ liability is limited to the amount unpaid on their shares. This means personal assets are protected in case of business failure.

Separate Legal Entity: A Pvt Ltd company is legally distinct from its shareholders, meaning it can enter into contracts, own property, and sue or be sued in its own name.

Restricted Share Transfer: Shares of a private limited company cannot be traded on a public stock exchange, and their transfer is limited to specific rules.

Minimum Shareholders and Directors: A private limited company can be formed with just two shareholders and two directors, with a maximum of 200 shareholders.

Why Choose a Private Limited Company for Your Business?

Credibility: Having a Private Limited Company Registration in India boosts the credibility of your business, making it easier to attract investors, raise capital, and enter into partnerships.

Limited Liability Protection: Unlike sole proprietorships and partnerships, the shareholders’ personal assets are not at risk in the event of the company’s debts or liabilities.

Tax Benefits: A Pvt Ltd company is eligible for various tax exemptions and deductions under the Income Tax Act, which helps reduce the overall tax burden.

Ease of Fundraising: A Pvt Ltd company can raise capital through the issuance of shares to investors, which is not possible in other business structures like a partnership.

Incorporation of a Private Limited Company Under the Companies Act 2013

The Companies Act 2013 governs the incorporation and operation of companies in India. The process of incorporating a Private Limited Company involves several legal steps to ensure that the company is established as per the provisions of this Act. Here’s a step-by-step guide on how to register a company in India:

Step 1: Choose a Suitable Name for Your Company

The first step is to select a unique name for your Private Limited Company that complies with the guidelines set by the Ministry of Corporate Affairs (MCA). The name must not be identical to an existing company, nor should it infringe upon any trademarks. The name should also reflect the company’s business objectives.

Step 2: Obtain Digital Signature Certificate (DSC)

All documents related to Company Registration in India need to be signed digitally. Therefore, the directors and shareholders of the company must obtain a Digital Signature Certificate (DSC), which is issued by government-authorized certifying agencies.

Step 3: Apply for Director Identification Number (DIN)

The next step is to obtain a Director Identification Number (DIN) for all proposed directors of the company. DIN is a unique number issued by the Ministry of Corporate Affairs, which is mandatory for anyone wishing to act as a director in an Indian company.

Step 4: Draft the Memorandum and Articles of Association (MOA & AOA)

The Memorandum of Association (MOA) defines the company’s objectives, while the Articles of Association (AOA) lays down the rules and regulations for its internal management. These documents must be drafted and signed by the directors and shareholders.

Step 5: Filing the Incorporation Application

Once the MOA and AOA are ready, the incorporation application is filed with the Ministry of Corporate Affairs (MCA) through the MCA portal. This is done by submitting the necessary forms, including SPICe+ (Simplified Proforma for Incorporating Company Electronically), which covers multiple services like name reservation, incorporation, and PAN and TAN applications.

Step 6: Issuance of Certificate of Incorporation

Once the application is verified and approved, the Registrar of Companies (RoC) will issue a Certificate of Incorporation, confirming the legal existence of the company.

Key Documents Required for Private Limited Company Registration

To register a private limited company, certain documents must be submitted, including:

Proof of Identity: PAN card, Aadhar card, passport, or voter ID of the directors.

Proof of Address: A recent utility bill or rental agreement for the registered office address.

Photographs: Passport-sized photos of all directors.

MOA & AOA: The company’s memorandum and articles of association.

DIN & DSC: Director Identification Number (DIN) and Digital Signature Certificate (DSC) for all directors.

How to Register a Startup Company in India?

Startups looking to incorporate a Private Limited Company have a simplified process through the Startup India initiative. This program offers various benefits, such as tax exemptions and easier compliance, for eligible startups. The registration process remains the same, but certain benefits are available to encourage innovation and entrepreneurship.

Register as a Startup: A company must be recognized as a startup by the Department for Promotion of Industry and Internal Trade (DPIIT).

Tax Exemptions: Eligible startups can avail of income tax exemptions for the first three years.

Simplified Compliance: The startup scheme offers easier regulations, allowing for fewer compliance requirements in the initial years.

Company Registration Online in India

With the increasing digitization, registering a company in India has never been easier. Company Registration Online in India is a hassle-free process that can be done from the comfort of your home or office. By visiting the MCA portal, entrepreneurs can submit their forms, track the progress, and complete the registration process online. The Company Registration Online in India system has significantly reduced paperwork and made the process faster and more efficient.

Conclusion

Incorporating a Private Limited Company under the Companies Act 2013 offers significant advantages to entrepreneurs, including limited liability protection, ease of raising capital, and enhanced credibility. If you are considering starting a business, the Pvt Ltd Company Registration in India is the ideal route for you. With the option to register a company in India online, the process has been made simpler and more efficient than ever before.

If you’re unsure of the procedure or need assistance, seeking professional advice from experts in Company Registration in India and Private Limited Company Registration in India can make the process smoother. Whether you’re a first-time entrepreneur or a seasoned businessperson, registering a startup company in India has never been more accessible.

Take the first step today and register your company in India to bring your entrepreneurial dreams to life!

India’s investment landscape has undergone a significant transformation over the last few decades. Traditional investment avenues like fixed deposits and public sector bonds are now complemented by a host of innovative investment options, one of the most popular beingAlternative Investment Funds (AIFs). These funds have grown in importance due to their ability to provide higher returns through investments in unlisted securities, private equity, hedge funds, venture capital, real estate, and other non-traditional assets.

However, in order to operate legally and attract investors, an AIF must be properly registered with the Securities and Exchange Board of India (SEBI). The registration process, though rewarding, can be complex, and it’s essential to understand the steps involved in the AIF Registration in India. In this blog, we’ll explore the process of AIF Registration Online in India, the categories of AIFs, and how an AIF Registration Consultant can help streamline the registration process.

What is an Alternative Investment Fund (AIF)?

An Alternative Investment Fund (AIF) is a privately pooled investment vehicle that collects funds from investors and makes investments in assets that are not typically available through conventional investment options like mutual funds or stocks. AIFs are designed to invest in ventures, assets, and projects that may be high-risk but also have the potential for high returns.

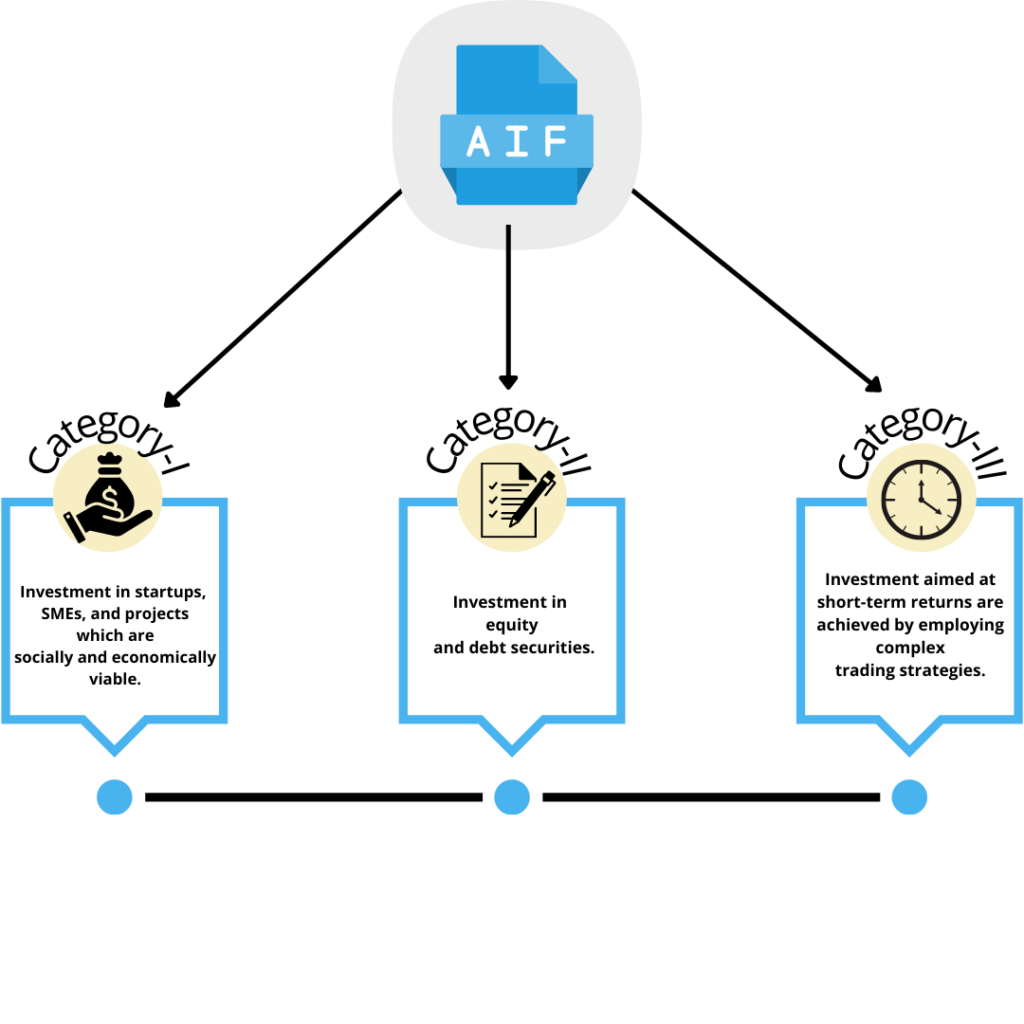

There are three categories of AIFs as regulated by SEBI:

Category I AIFs: Funds that invest in sectors or areas that are considered economically and socially beneficial, such as venture capital funds, social venture funds, and infrastructure funds.

Category II AIFs: Funds that do not take excessive risks and do not use leverage in their operations, like private equity funds and debt funds.

Category III AIFs: These include funds that employ complex strategies and use leverage for higher returns, such as hedge funds.

Why is AIF Registration Necessary in India?

For an AIF to raise capital, invest on behalf of investors, and manage assets, it needs to be registered with SEBI. TheAIF Registration in India serves to:

Ensure transparency and accountability in the functioning of the fund.

Safeguard investor interests by enforcing strict regulatory norms.

Enhance credibility by ensuring compliance with Indian laws.

Without proper registration, any fund offering investments as an AIF will be considered illegal and cannot legally raise funds from investors. Therefore, the AIF Registration Process is essential for establishing the fund’s credibility and operational legality.

Steps to Register as an AIF in India

The process of AIF Registration Online in India follows a set sequence, requiring thorough documentation and compliance with SEBI’s regulations. Let’s break down the major steps involved in AIF Registration in India.

1. Determine the Type of AIF

Before proceeding with AIF Registration Online in India, the first crucial step is deciding which category of AIF best fits your fund’s objectives and strategies. Here’s a brief overview:

Category I AIFs: These include funds that support new ventures, social causes, and infrastructure projects. This category usually benefits from some tax advantages and lighter regulatory scrutiny.

Category II AIFs: Funds in this category invest in private equity or debt instruments and employ moderate risk. These funds are required to adhere to more stringent norms.

Category III AIFs: These funds use leverage, short-selling, and other complex investment strategies to maximize returns, usually targeting sophisticated investors.

Choosing the right category is critical because it impacts the structure, investment policies, risk factors, and regulatory requirements that will apply to the fund.

2. Understand the Eligibility Criteria for AIF Registration

To qualify for AIF Registration in India, the fund must meet certain eligibility requirements. These include:

Fund Manager Requirements: The fund manager must be a registered entity, typically a company, and must possess relevant experience and qualifications to manage an AIF.

Minimum Investment Requirement: The minimum corpus for an AIF is generally ₹20 crore. However, the total corpus may vary depending on the category and other specific criteria.

Investor Requirements: An AIF can only accept funds from certain types of investors, typically high-net-worth individuals (HNIs) or institutional investors.

In addition, the fund must have clear governance, risk management policies, and a defined investment strategy.

3. Prepare the Documentation

The AIF Registration in India requires a comprehensive set of documents to be submitted to SEBI. These typically include:

Constitutional Documents: The memorandum of association (MOA), articles of association (AOA), and partnership deed (for a limited liability partnership or LLP).

Details of the Fund Manager: The qualifications and professional background of the fund manager and the management team.

Investment Strategy and Policies: A detailed outline of the fund’s investment approach, including target sectors, asset allocation, and risk management strategies.

Financial Statements: Projections of the fund’s financial performance, including balance sheets and profit & loss accounts.

Once the documentation is ready, it must be submitted to SEBI through their online platform.

4. Registering the AIF Online with SEBI

The next step is to proceed with Online AIF Registration in India. SEBI has set up a dedicated online portal for AIF registration, making it easier to submit applications and documents. Here’s how you can proceed:

Create an Account: Visit the SEBI website and create an account with the appropriate login credentials.

Submit the Application Form: Complete the online application form, providing accurate and up-to-date details about the fund, its objectives, and the fund manager’s experience.

Upload Supporting Documents: Upload all the necessary documents such as the constitutional documents, fund manager qualifications, and investment policies.

Pay the Fees: The registration process requires payment of a fee, which varies depending on the fund category.

5. Review and Approval by SEBI

After submitting the application and documents, SEBI will carry out due diligence to verify the authenticity and completeness of the information provided. The regulator may request additional documents or clarifications. Once satisfied, SEBI will approve the registration.

The approval process typically takes a few weeks to months, depending on the complexity of the application and the fund’s structure. Once SEBI grants approval, the AIF will receive a certificate of registration, and the fund can legally begin raising capital and making investments.

Role of an AIF Registration Consultant

Given the complexities of the AIF Registration Process and the stringent regulatory requirements, many fund managers opt to work with an AIF Registration Consultant. Here’s how a consultant can help:

Advisory Services: An AIF Registration Consultantcan advise you on which AIF category best suits your investment strategy, helping you understand the regulatory nuances and financial implications of each option.

Document Preparation: The consultant can assist in preparing the necessary documentation for the registration process, ensuring that all forms are filled out correctly and comply with SEBI’s guidelines.

Online Application Filing: With their experience, AIF registration consultants are well-versed in the AIF Registration Online in India process and can ensure that the online filing is accurate and timely.

Compliance Management: An AIF registration consultant can provide ongoing support to ensure that the fund remains compliant with SEBI regulations even after the registration process is complete. This helps to avoid penalties and operational disruptions.

6. Taxation and Ongoing Compliance

Once your AIF is successfully registered, it is essential to understand the taxation and ongoing compliance requirements. Different categories of AIFs have different tax implications, and failure to comply with regulatory norms can lead to severe penalties. A consultant can help you navigate these post-registration requirements.

Conclusion

The process of Alternative Investment Fund Registration in India is crucial for any fund that aims to attract investment and manage capital in a regulated manner. With the Online AIF Registration in India making the process faster and more accessible, registering an AIF has become easier, though it still requires careful attention to legal and regulatory details.

By understanding the registration process and enlisting the help of an AIF Registration Consultant, fund managers can ensure that their AIF is legally compliant, operationally sound, and poised for success in India’s dynamic investment landscape.

Whether you are launching a venture capital fund, a private equity fund, or a real estate fund, understanding how to get registered as an AIF in India is the first step in making your fund a reality.

Quick answer: How long does AIF registration take?

SEBI does not prescribe a guaranteed overall period for granting Alternative Investment Fund registration. As a practical planning estimate, applicants should generally allow approximately three to six months from preparation to receipt of the registration certificate.

The process can take longer—sometimes six months or more—if the application is incomplete, the fund structure is complex, the sponsor or investment manager does not clearly meet regulatory requirements, or responses to SEBI’s queries are delayed.

SEBI’s published guidance states that an applicant will generally receive an initial reply within 21 working days after submitting an application. This does not mean the registration will be granted within 21 working days. The final timeline depends substantially on how quickly and satisfactorily the applicant responds to regulatory requirements and observations. SEBI’s AIF registration guidance

Understanding SEBI AIF registration

An Alternative Investment Fund, or AIF, is a privately pooled investment vehicle that collects capital from sophisticated investors and invests according to a defined investment policy.

AIFs in India are regulated under the Securities and Exchange Board of India (Alternative Investment Funds) Regulations, 2012. The regulations were most recently amended on July 14, 2026. Current SEBI AIF Regulations

An applicant may seek registration under one of three broad categories:

Category I AIF: Includes venture capital funds, infrastructure funds, social impact funds and other funds considered economically or socially desirable.

Category II AIF: Commonly includes private equity funds, debt funds and other funds that do not undertake leverage except for permitted operational requirements.

Category III AIF: Includes funds that may use complex trading strategies and leverage, subject to applicable conditions.

The category selected affects the fund’s investment strategy, regulatory obligations and the information SEBI may examine during registration.

Estimated SEBI AIF registration timeline

A well-prepared AIF registration can be divided into the following stages:

Registration stage

Indicative time

Fund planning and category selection

1–2 weeks

Formation of the fund and manager entities

2–4 weeks

Drafting legal and regulatory documents

3–6 weeks

Filing the application on the SEBI portal

2–5 working days

Initial review or communication from SEBI

Generally within 21 working days

Responding to SEBI observations

2–8 weeks or longer

In-principle approval and payment of fees

1–3 weeks

Grant of registration certificate

Depends on satisfactory compliance

Typical end-to-end planning estimate

3–6 months

These periods are planning estimates, not statutory guarantees. Several stages may also run simultaneously.

Stage 1: Planning the AIF structure

Estimated time: One to two weeks

The registration journey begins before any application is filed. The sponsor and proposed investment manager must first determine:

The investment objective of the fund

The appropriate AIF category and subcategory

The legal structure of the fund

Target investors

Proposed fund corpus

Sponsor commitment

Management and governance structure

Investment and exit strategy

Proposed tenure of the scheme

Whether the fund will use borrowing or leverage

Key service providers

An AIF may generally be established as a trust, company, limited liability partnership or body corporate. In practice, many Indian AIFs use a trust structure, but the correct structure depends on taxation, governance, investor expectations and the commercial model.

Making major changes after the application has been submitted can lead to additional questions, document revisions and delays. It is therefore important to finalise the commercial and legal structure at the beginning.

Stage 2: Establishing the fund and investment manager

Estimated time: Two to four weeks

Once the structure has been selected, the relevant entities and arrangements must be established. Depending on the chosen structure, this may include:

Formation of the trust, company or LLP

Execution and registration of the trust deed

Incorporation or establishment of the investment manager

Appointment of the trustee, where applicable

Finalisation of ownership and control

Appointment of directors, partners or designated partners

Establishment of an appropriate office and operational infrastructure

Opening of bank accounts

Obtaining PAN and other registrations

Preparation of board or partner resolutions

The exact time will depend on the legal form, availability of documents, name approvals and coordination among the sponsor, manager, trustee and professional advisers.

Stage 3: Preparing the AIF registration documents

Estimated time: Three to six weeks

Documentation is frequently the most demanding stage of the AIF registration process. SEBI examines more than the existence of the fund entity. It also considers whether the proposed sponsor and manager are suitable, adequately experienced and capable of operating a regulated investment fund.

The application package may include:

Form A

Constitutional documents of the applicant

Trust deed, LLP agreement or memorandum and articles of association

Details of the sponsor and investment manager

Shareholding and ownership structure

Financial statements and net-worth evidence

Details of directors, partners and key investment personnel

Professional qualifications and investment-management experience

Infrastructure and staffing details

Disciplinary and litigation declarations

Investment strategy and risk-management framework

Draft Private Placement Memorandum

Compliance policies

Due-diligence declarations and supporting documents

Details of affiliates and group entities

SEBI’s January 2025 registration FAQs provide an application checklist and explain that applications must be filed through the SEBI Intermediary Portal. The stated application fee is ₹1,00,000 plus applicable GST. SEBI FAQs for grant of AIF registration

Registration fees payable after approval vary according to the AIF category. Applicants should verify the latest fees and applicable taxes at the time of filing.

Stage 4: Filing the application with SEBI

Estimated time: Two to five working days after the documents are ready

The applicant must submit the registration application through the SEBI Intermediary Portal. The applicant receives login credentials and uses the “Fresh Registration” option under the AIF section to complete the filing.

Before submission, applicants should verify that:

Form A is complete and consistent

Names and addresses match constitutional records

Supporting documents are properly executed

Financial information is updated

The AIF category matches the proposed investment strategy

Sponsor and manager details are fully disclosed

The Private Placement Memorandum is consistent with the application

The application fee has been paid correctly

Required declarations have been signed by authorised persons

Even a technically minor inconsistency can result in a regulatory query. For example, different descriptions of the investment strategy in Form A and the PPM may require clarification or revision.

Stage 5: SEBI’s initial review

Indicative response: Generally within 21 working days

SEBI’s published guidance states that an applicant will generally receive a reply within 21 working days of submitting the application. Applicants should interpret this carefully.

The 21-working-day period generally relates to an initial regulatory communication. SEBI may:

Seek additional information

Point out missing documents

Ask for clarification of the investment strategy

Request changes to the fund structure

Examine the experience of key personnel

Seek evidence of the manager’s operational capabilities

Ask questions about affiliates or past business activities

Require revisions to the PPM

Seek clarification about sponsor commitment or net worth

Therefore, receiving a reply within 21 working days is not the same as obtaining final registration within that period.

Stage 6: Responding to SEBI observations

Estimated time: Two to eight weeks, but potentially longer

This stage has the greatest influence on the overall registration timeline. The speed of approval often depends on the quality of the application and the applicant’s ability to respond quickly and accurately.

A strong response should:

Address every observation separately

Use clear and direct language

Include revised documents where required

Highlight changes made in each document

Ensure that all revised documents remain consistent

Include supporting evidence rather than unsupported statements

Be approved by the relevant sponsor, manager or governing body before submission

If the first response is incomplete, SEBI may issue another round of observations. Multiple rounds of queries can extend the registration timeline considerably.

Applicants should maintain a central response tracker showing each SEBI observation, the proposed response, the responsible person, required supporting documents and submission status.

Stage 7: Approval, registration fee and certificate

Once SEBI is satisfied that the applicant meets the regulatory requirements, it may approve the application and ask the applicant to pay the applicable registration fee.

After payment and completion of the required formalities, SEBI may grant the certificate of registration.

The fund must ensure that its subsequent activities remain within the scope of the category and conditions under which registration was granted.

Does the GARUDA mechanism make AIF registration faster?

SEBI introduced the Green-Channel: AIF Rollout Upon Document Acknowledgement, or GARUDA, mechanism through a circular dated July 30, 2026. The mechanism is intended to streamline the processing and launch of AIF schemes by relying more heavily on prescribed due diligence and declarations. SEBI GARUDA circular

However, applicants should distinguish between:

Registration of the AIF itself; and

Filing and processing of the scheme’s Private Placement Memorandum.

GARUDA primarily relates to the processing and rollout of schemes. It does not mean that every new AIF registration will automatically be completed within a fixed green-channel period.

For the first scheme, scheme launch remains connected to the grant of AIF registration. Accordingly, the applicant must still satisfy SEBI regarding its eligibility, structure, sponsor, manager, key personnel and other registration requirements.

What can delay SEBI AIF registration?

1. An incomplete application

Missing annexures, unsigned documents, outdated financial statements or incomplete declarations commonly lead to additional observations.

2. Inconsistency between documents

SEBI may seek clarification if Form A, the trust deed, investment management agreement and PPM describe the fund differently.

3. Unclear investment strategy

Broad statements such as “investing in growth opportunities” may not adequately explain the proposed asset classes, sectors, investment stages, geography, risk controls and exit strategy.

4. Insufficient experience of the investment team

SEBI may examine whether the investment manager and key personnel possess suitable professional qualifications and relevant experience.

5. Complex ownership structures

Multiple layers of holding companies, foreign shareholders or unclear beneficial ownership may increase the level of regulatory scrutiny.

6. Sponsor or manager eligibility issues

Questions concerning net worth, fit-and-proper status, prior regulatory matters, litigation or disciplinary history can lengthen the review.

7. Weak operational readiness

The manager must demonstrate that it has adequate infrastructure, personnel, compliance arrangements and systems to manage the AIF.

8. Delayed responses to SEBI

If the applicant takes several weeks to respond to each observation, the registration process will naturally take longer.

9. Frequent commercial changes

Changing the fund category, sponsor, manager, investment strategy or legal structure during regulatory review may require substantial revisions.

10. Deficiencies in the PPM

Inaccurate, incomplete or inconsistent disclosures in the Private Placement Memorandum can delay the process and create regulatory risk.

How can applicants complete AIF registration faster?

No consultant or applicant can guarantee a specific approval date because registration remains subject to SEBI’s review. However, the following steps can reduce avoidable delays:

Complete a regulatory readiness assessment

Review the sponsor, manager, key personnel, ownership structure and investment proposal against the applicable AIF requirements before filing.

Finalise the structure early

Select the fund category, legal structure, investment strategy, sponsor and manager before preparing the application.

Use a comprehensive document checklist

Create a checklist based on the latest SEBI regulations, master circulars, FAQs and portal requirements.

Keep all documents consistent

Use identical descriptions of the fund, parties, strategy, tenure, corpus and governance arrangements throughout the application.

Prepare for regulatory questions

Anticipate questions about the investment team, sponsor commitment, track record, beneficial ownership, risk management and conflicts of interest.

Assign a dedicated response team

A single team should coordinate information from legal, tax, finance, compliance and investment professionals.

Respond promptly and completely

A fast but incomplete response may create another round of questions. The objective should be to provide one comprehensive and well-supported response.

Can an AIF start raising money before receiving registration?

A proposed AIF should not represent itself as a SEBI-registered AIF before receiving its registration certificate.

Scheme launch and circulation of the PPM must also follow the applicable regulatory framework. The exact requirements may differ for regular schemes, accredited-investor-only schemes, angel funds and large value funds for accredited investors.

Applicants should examine the latest regulations and SEBI circulars before approaching investors or circulating offering documents.

Practical example of an AIF registration timeline

Consider a Category II private equity fund with an Indian sponsor and investment manager:

Weeks 1–2: The promoters finalise the fund structure, target corpus, investment strategy and key team.

Weeks 3–5: The fund entity and investment manager arrangements are established.

Weeks 4–8: Form A, constitutional documents, compliance policies and the PPM are prepared.

Week 9: The application is submitted through the SEBI portal.

Weeks 10–13: SEBI conducts its initial review and communicates observations.

Weeks 14–16: The applicant prepares and submits a detailed response.

Weeks 17–20: Additional clarifications, if any, are addressed.

Weeks 21–24: Approval, payment of registration fees and issuance of the certificate may follow, subject to SEBI’s satisfaction.

In this example, the overall process takes approximately five to six months. A simpler, exceptionally well-prepared application may move faster, while a complex application involving multiple observations may take longer.

Is there a guaranteed SEBI AIF registration timeline?

No. SEBI does not guarantee that every AIF registration application will be approved within a fixed number of days.

The regulator’s published guidance refers to an initial reply generally being issued within 21 working days. The final registration period depends on the completeness of the application, the complexity of the structure and the applicant’s speed in satisfying regulatory requirements.

Applicants should be cautious of anyone promising guaranteed approval within 21 days or any other fixed period.

Conclusion

A realistic timeline for completing SEBI AIF registration is generally three to six months, including preparation, filing, regulatory review, responses and approval formalities. Complex applications may take longer.

The most effective way to reduce delays is to submit a complete, consistent and well-supported application from the outset. Sponsors and fund managers should finalise their structure early, prepare clear disclosures and maintain a dedicated team for responding to SEBI observations.

BIATConsultant assists fund sponsors and investment managers with AIF structuring, document preparation, SEBI registration support, regulatory coordination and post-registration compliance. Professional preparation can help applicants identify potential issues before filing and move through the review process more efficiently.

Disclaimer: This article is intended for general informational purposes and does not constitute legal, tax, investment or regulatory advice. SEBI regulations, circulars, fees and portal requirements may change. Applicants should review the latest official requirements and obtain professional advice based on their proposed fund structure.

Frequently Asked Questions

How many days does SEBI take to register an AIF?

SEBI does not specify a guaranteed overall approval period. Its published guidance states that an applicant will generally receive an initial reply within 21 working days. Final registration may practically take around three to six months, depending on the application and responses to observations.

Can SEBI AIF registration be completed in one month?

It is generally not advisable to plan on completing the entire process in one month. Preparation of the entities, documents and PPM itself may take several weeks, followed by SEBI’s review and possible queries.

Why does AIF registration take several months?

The process involves scrutiny of the applicant, sponsor, investment manager, key personnel, fund structure, investment strategy, financial resources, regulatory history and offering documents.

What is the fastest way to obtain AIF registration?

The best way to avoid delay is to finalise the structure early, prepare a complete application, maintain consistency across all documents and respond comprehensively to SEBI’s observations.

Does the 21-working-day period mean automatic approval?

No. The period mentioned in SEBI’s guidance relates to a general response after receiving the application. It is not an automatic or guaranteed approval timeline.

Does the AIF category affect the registration timeline?

Yes. The category and strategy may affect the nature of SEBI’s review. Category III structures, complex strategies, leverage arrangements and unusual ownership structures may require additional explanation.

How long does Category II AIF registration take?

A Category II AIF should generally budget approximately three to six months for the complete process. The actual duration depends on documentation quality, structure and regulatory observations.

How long does Category III AIF registration take?

Category III registration may take three to six months or longer where the proposed strategy, leverage, risk controls or operational framework requires detailed review.

Can an AIF launch its first scheme immediately after filing?

Not necessarily. For a first scheme, launch remains linked to receipt of AIF registration and satisfaction of the applicable PPM filing requirements. Applicants must follow the latest SEBI regulations and circulars.

Is professional assistance mandatory for AIF registration?

Engaging a consultant is not, by itself, a substitute for meeting SEBI’s requirements. However, legal, tax, compliance and regulatory professionals can help structure the fund, prepare consistent documents and manage regulatory observations effectively.

India’s alternative investment fund market is grown significantly over the last few decades , making Alternative Investment Funds (AIFs) is one of the most preferred investment for the private firms, ventures, hedge funds and the institutional investors. To operate this legally in India, this AIF must contain registration from the Securities and Exchange Board of India (SEBI) SEBI (Alternative Investment Funds) Regulations, under 2012.

If you want plan for launching an investment fund in India, the understanding of AIF registration process is most important element for understanding AIF. This guide explains each step by step in detail.

What is an Alternative Investment Fund (AIF)?

An Alternative Investment Fund (AIF) is a specialized investment vehicle that pools capital from multiple investors to invest in non-traditional asset classes, such as private equity, real estate, hedge funds, venture capital, and commodities. These funds are typically managed by professional fund managers and are structured as limited partnerships or limited liability companies.

AIFs can be structured as:

Trusts

Limited Liability Partnerships (LLPs)

Companies

Body Corporates

These are the funds which are regulated by SEBI and are generally used for the investments in startups, private companies, infrastructure projects, real estate, private equity, venture capital, debt instruments, and hedge fund strategies.

Categories of AIFs in India

Before starting any registration process the fund managers has to choose the appropriate AIF category according to need.

Category I AIF

These are AIFs that invest on start up and early stage venture , small and medium enterprises , infrastructure . AIFs I also Include investment in social and economically desire group. Category I considered to have moderate risk and low regulatory restriction compare to other AIFs categories.

Examples:

Venture Capital Funds

Angel Funds

Infrastructure Funds

SME Funds

Social Venture Funds

Category II AIF

These are AIFs that do not fall under both categories AIFs I and AIFs II . This category known for moderate risk and uncertainites for investment . These category include private Equity funds , debt funds , and funds invest in real state among India.

Examples:

Private Equity Funds

Debt Funds

Fund of Funds

Category III AIF

Category III Use complex stragies for These are AIFs that use complex trading strategies and leverage to generate high returns for investors, such as hedge funds, among others.

Step-by-Step AIF Registration Process in India

Step 1: Determine the Fund Structure

The first step is decide the legal structure of the fund for investment process.

And determining whether the funds fall in which category either is category I , II, Or III . Choosing the correct category is critical because regulatory requirements differ for each category.

You must:

Create the trust, LLP, or company

Draft constitutional documents

Obtain PAN and other registrations

Establish the investment management entity

SEBI reviews the legal structure carefully before granting approval.

Step 2: Select the Appropriate AIF Category

The second step is to determine whether the the fund falls under which is it Category I, Category II, or Category III.

The category affects investment restrictions, compliance requirements, and operational guidelines. Selecting the correct category at the beginning helps avoid regulatory complications later.

Step 3: Appoint the Sponsor and Investment Manager

Every AIF requires a sponsor and an investment manager for the analyising of funds.

The sponsor establishes the fund and contributes the required continuing interest, while the investment manager is responsible for managing investments and making portfolio decisions.

SEBI reviews the qualifications, experience, and regulatory track record of these entities during the registration process.

Step 4: Draft the Private Placement Memorandum (PPM)

The Private Placement Memorandum (PPM) is one of the most important documents for the AIF registration in India.

It contains key information such as:

Investment strategy for the investors

Risk factors and uncertainty

Governance structure

Fee structure

Investor rights

Exit mechanisms

A well-drafted PPM improves transparency and increases the likelihood of regulatory approval.

Step 5: Prepare Documentation

The Applicants must have all the documents which are needed for the investment before filing the application.

Common documents include:

Trust Deed or LLP Agreement

Certificate of Incorporation

PAN card details

Bank account details

Sponsor information

Investment manager details

Financial statements

Compliance declarations

Private Placement Memorandum

Accurate documentation helps prevent delays during SEBI review.

Step 6: Submit the Application to SEBI

This is one of the most important key element of the AIFs registration because application is officially submitted and the review as well as approval will be done SEBI. The application for AIF registration is submitted through SEBI’s online intermediary portal. The document should well prepared for the delay of registration.

The applicant must complete Form A, upload supporting documents, and pay the applicable fees.

Once submitted, SEBI begins its review process.

Step 7: Respond to SEBI Queries

Before the approval the SEBI may seek clarifications regarding the fund structure, investment strategy, governance framework, or the documentation.

Timely and accurate responses are essential for smooth approval.

Step 7: Respond to SEBI Queries

These is the final step SEBI will ask for the document clarification regarding several step for the investment. Respond to SEBI Queries objective is to ensure that the proposed Alternative Investment Fund complies with all regulatory requirements and adequately protects investor interests. In these several Queries may ask :

Asking for the missing documents , clarification regarding the fund structure, Investors protection, Governance and compliance framework concern.

How Long Does AIF Registration Take?

The time taken for AIF registration process depends on the situation of complexity of the application and the quality of documentation that has been submitted.

In most cases:

Fund Structuring: 2–4 Weeks

Documentation Preparation: 3–6 Weeks

SEBI Review: 4–12 Weeks

Final Approval: 2–4 Weeks

Most AIF registrations are completed within 2 to 8 months.

Conclusion

AIFs is very important crucial step for every fund manager , venture capital funds ,private equity funds and investment professionals looking to establish a regulated investment platform in India. By selecting the best AIFs category , fund structure , preparing all the documents and analysing the document which is needed for the AIFs registration process. By selecting the appropriate fund structure, preparing robust documentation, drafting a comprehensive PPM, and complying with SEBI regulations, applicants can successfully launch and operate an Alternative Investment Fund.

Frequently Asked Questions (FAQs)

What is a SEBI AIF Registration?

An Alternative Investment Fund that has registered with the Securities and Exchange Board of India (SEBI) is known as a SEBI AIF Registration. AIFs are investment vehicles that invest in assets such as private equity, venture capital, real estate, and debt securities.

What is AIF Registration?

All the registration process are done and approval from the SEBI is most important . In these approval from SEBI to establish and operate an Alternative Investment Fund in India.

Is SEBI Registration Mandatory for AIFs?

Yes, it is very important in every Alternative investment funds, and must be register with SEBI.

Who Can Register an AIF in India?

A Trust, LLP, Company, or Body Corporate can apply for AIF registration subject to SEBI regulations.

How Long Does AIF Registration Take?

It takes almost 2-8 months according to document submission to SEBI. If any document is not missing it will approve soon.

What is a Private Placement Memorandum (PPM)?

A PPM is a legal document that outlines the fund’s investment strategy, risks, fee structure, governance, and investor rights.

What Are the Benefits of AIF Registration?

AIF registration provides regulatory recognition, investor confidence, fundraising opportunities, and a structured framework for managing investments.

There is more than Alternative Investment Funds (AIFs) which have become the most one of the preferred investment vehicles for the high-net-worth individuals (HNIs), family offices, institutional investors, and startups are looking for the well structured capital solutions in India.There are many investors and businesses who are still in doubt to understand the difference between Category I, Category II, and Category III AIFs.

If someone is planning to invest in AIFs, and want to launch an investment fund, or explore emerging AI-driven investment technologies, understanding these categories are very important for making informed financial decisions.

In this guide, we will try to explain everything about Category I, II, and III AIFs in a very simple language — including the structure, benefits, taxation, regulations, examples, and how technology and AI are transforming the AIF ecosystem.

What is an AIF?

There is An Alternative Investment Fund (AIF) is a privately pooled investment vehicle regulated by the Securities and Exchange Board of India (SEBI). The funds used to collect money from the sophisticated investors and invest in assets beyond traditional stocks and bonds.

AIFs generally invest in:

Startups company

Private equity

Venture capital

Real estate

Infrastructure development

Debt instruments

Hedge funds

AIFs is regulated by the SEBI (Alternative Investment Funds) under the Regulations, 2012.

Types of AIFs in India

The SEBI is classified in AIFs in three categories

Category I AIF

Category II AIF

Category III AIF

Every category has different investment strategies like risk levels, tax implications, and the regulatory benefits.

Category I AIF Explained

The Category I AIFs invest in those sectors which are considered socially and economically beneficial for India.

These kinds of funds receive more incentives and support from the government because this sector contribute to economic growth as well as innovation.

Key Features of Category I AIFs

Invest in the startups in the Newly businesses

The promotion of the Entrepreuneurship

Have less investment risk

Government incentives may apply

Long-term investment opportunity

Types of Category I AIFs

Venture Capital Funds (VCFs)

Investing in the startups and the high-growth companies.

SME Funds

These are focused in Medium enterprise

Infrastructure Funds

In these Investment in the infrastructure project for example Roads , energy and logistics.

Social Venture Funds

In these the company which creates social welfare gets Funds

Who Should Invest in Category I AIFs?

Category I AIFs are suitable for:

For the Long-term investors

Startup-focused investors which can create innovation

Investors seeking government-supported sectors

High-risk, high-growth investors

Category II AIF Explained

Category II AIFs are the most common type of AIF in India. These kinds of funds don’t receive incentive through the the government and do not have aggresive trading strategies compare to Category III.

They primarily invest in the private companies, debt instruments, and the unlisted businesses.

Features of Category II AIFs

There is no leverage expectation for operations.

Mature business gets investment

From medium to long term investment

It is Stable compared to Category III

Widely used by private equity firms

Different types of Category II AIFs

Private Equity Funds

Private companies which is established gets Investment

Debt Funds

Invest in debt for securities of companies.

Fund of Funds

Invest in other AIFs.

Real Estate Funds

Invest in commercial and residential projects.

Who Should Invest in Category II AIFs?

Ideal for:

High Net worth individual

Institutional investors

Family offices

Investors seeking balanced risk and return

Category III AIF Explained

In Category III AIFs they use high complex trading strategies and may employ leverage to generate short-term investment returns.

These funds are similar to the hedge funds and actively trade across markets.

Features of Category III AIFs

Use for leverage and derivatives

High risk for investment

Short-term opportunities for trading

Higher flow of liquidity

Suitable for sophisticated investors

Examples of Category III AIFs

Hedge Funds : wide range of assets , debt , real estates

Quantitative Trading Funds

AI-powered Algorithmic Trading Funds

Long-short equity funds

Who Should Invest in Category III AIFs?

Suitable for the :

Aggressive investors

HNIs

Institutional traders

Investors comfortable with market fluctuations of price

Difference Between Category I, II, and III AIFs

Feature

Category I AIF

Category II AIF

Category III AIF

Investment Focus on

Startups, SMEs, infrastructure

Private equity, debt

Trading & hedge strategies

Government Incentives presence

Yes

No

No

Risk Level

Moderate to High

Moderate

Very High

Leverage Allowed

Limited

Limited

Yes

Investment time period

Long-term

Medium to Long-term

Short-term to Medium-term

Liquidity

Low

Moderate

High

Type of investor

Growth investors

Balanced investors

Aggressive investors

Examples:

Venture capital funds

PE funds

Hedge funds

Taxation of AIFs in India

Taxation differs depending on the category of the AIF.

Category I and II AIF Taxation

These are categories who generally enjoy pass-through taxation status, meaning income is taxed in the hands of investors rather than the fund itself.

Category III AIF Taxation

Category III do not receive any pass through status and are taxed at their fund level.

Tax regulations can change frequently, so professional tax consultation is advisable.

According to SEBI regulations:

Minimum investment should be 1 crore rupee for the investor.

And For the directors/employees/managers of the fund should be 25 lakhs.

These are mainly designed for sophisticated investors.

Benefits of Investing in AIFs

Portfolio Diversification

In AIFs we explore beyond traditional equity and also for the debt markets.

Access to High-Growth Opportunities

Investors can directly participate in startups, private companies, and emerging sectors for the high return.

Fund Management by professional

It is Managed by experienced professionals and investment experts to reduced the risk and uncertainties of your funds.

Potential for Higher Returns

Alternative assets can be generated higher returns compare to conventional investments.

Risks Associated with AIFs

AIFs offer strong growth potential, they also come with high risks:

Limited liquidity

Market uncertainty

Government Regulation

High minimum investment

Complex structures

Investors should evaluate their risk appetite more carefully before investment in company.

How AI is Transforming the AIF Industry

Artificial Intelligence is changing very fast the way Alternative Investment Funds operate.

Modern AIF firms are using AI for:

Portfolio optimization

For identifying the risk

Detection of funds

Predictive analytics

Algorithmic trading

Investor reporting automation

AI agents can process a huge financial datasets in real-time, helping the fund managers make faster decision and more reliable investment decisions.

Businesses looking to integrate intelligent automation into investment operations can leverage custom AI solutions from Winklix AI Agent Development Services. Their AI-driven systems help enterprises build autonomous AI agents for finance, investment management, and operational automation.

Why Understanding AIF Categories Matters

Choosing the right AIF category depends on several factors:

Investment goals

Risk tolerance

Liquidity requirements

Tax planning

Investment horizon

A startup-focused investor may prefer Category I, while a stable private equity investor may choose Category II. Aggressive investors looking for high-frequency strategies may opt for Category III.

Understanding these differences helps investors make smarter financial decisions.

Future of AIFs in India

India’s alternative investment market is expected to grow further in future due to significantly aspects:

Rising the ecosystem

Due to Increased HNI participation

The growth of the private capital

AI-driven investment management

Increase of fintech and wealthtech platforms

As the financial technology is evolving, AI -powered fund management and automation is likely to become more in future of AIFs .

Final Thoughts

Alternative Investment Funds are reshaping India’s investment landscape by offering sophisticated investors access to private markets, startups, and advanced trading opportunities.

The understanding of difference between Category I, II, and III AIFs is very important key aspects before making any investment decisions. Each and every category serves different investor needs, risk profiles, and financial goals.

As AI automate and continue to transform financial services, the future of AIF management will become more increasingly data-driven and intelligent. Businesses and investment firms are adopting AI-powered solutions early will gain a strong competitive advantage in the evolving alternative investment ecosystem.

Frequently Asked Questions (FAQs)

1. What is the main difference between Category I, II, and III AIFs?

Category I focuses on startups and socially beneficial sectors, Category II focuses on private investment and debt investments, while Category III invest in complex trading and hedge fund strategies.

2. Which AIF category is the safest?

The category II AIFs are find safe and considered relatively stable for the investment.Category III is avoided because of leverage trading strategies .

3. Can Category III AIFs use leverage?

Yes, Category III AIFs are allowed to use leverage and derivatives for investment strategies.

4. What is the minimum investment required for AIFs in India?

The minimum investment amount is generally ₹1 Crore per investor.

5. Are AIFs regulated in India?

Yes, AIFs are regulated by the (SEBI)Securities and Exchange Board of India

6. Which AIF category invests in startups?

The Category I AIFs primary focus on investment in startups, SMEs, and innovative driven businesses.

7. How is AI being used in AIF management?

AI helps in many aspects like prediction analytics, algorithmic trading, investor analytics, portfolio management, and automation of investment operations.

8. Are AIFs better than mutual funds?

AIFs offer access to alternative assets and potentially higher returns, but they also comes with the higher barrier risk and it take larger investments compared to mutual funds.

Non-Banking Financial Companies (NBFCs) play a crucial role in India’s financial ecosystem by providing credit to underserved segments, SMEs, and individuals. However, managing credit risk and predicting loan defaults remain significant challenges. With the advancement of technology, Artificial Intelligence (AI) has emerged as a powerful tool helping NBFCs enhance risk assessment, reduce defaults, and improve overall portfolio performance.

Understanding Loan Default Risks in NBFCs

Loan defaults can severely impact an NBFC’s profitability and regulatory standing. Traditional credit assessment models often rely on limited historical data and manual evaluation, which may not accurately capture borrower behavior. As regulatory scrutiny increases—especially for companies holding an NBFC license from RBI in India—adopting smarter risk management practices has become essential.

How AI Transforms Loan Default Prediction

AI-driven systems analyze vast amounts of structured and unstructured data to identify patterns that humans might miss. By leveraging machine learning algorithms, NBFCs can predict potential defaults with higher accuracy and speed.

AI helps NBFCs by:

Analyzing customer transaction behavior in real time

Evaluating alternative data such as digital footprints and spending habits

Detecting early warning signals of repayment stress

Continuously improving credit models through learning algorithms

These capabilities significantly enhance credit decision-making and portfolio quality.

Benefits of AI for NBFCs

The integration of AI in credit risk management delivers multiple advantages:

Improved accuracy in credit scoring

Faster loan approval processes

Reduced operational costs

Better compliance with RBI regulations

Lower non-performing assets (NPAs)

These benefits strengthen the credibility of NBFCs operating under an NBFC license online framework.

AI and Regulatory Compliance for NBFCs

As NBFCs adopt AI-driven systems, compliance with regulatory guidelines remains critical. Whether it is NBFC registration online or ongoing regulatory reporting, AI helps streamline compliance by automating documentation, monitoring risk exposure, and ensuring transparency in decision-making.

For new entrants, completing NBFC Registration online in India becomes smoother when technology-driven processes are aligned with regulatory requirements.

Importance of Expert Guidance in NBFC Registration

Setting up an NBFC involves complex legal and compliance procedures. Engaging a professional NBFC registration consultant or an experienced NBFC Registration Consultant in India ensures that licensing, capital requirements, and RBI approvals are handled efficiently.

Consultants also guide NBFCs in adopting technology frameworks, including AI-based risk assessment tools, after securing an NBFC license from RBI in India.

Why AI Adoption Is the Future for NBFCs

AI is no longer optional for NBFCs—it is a strategic necessity. With increasing competition and tighter regulations, NBFCs that leverage AI gain a strong advantage in managing credit risk, improving customer trust, and achieving sustainable growth.

Whether you are planning NBFC registration online or scaling an existing NBFC, integrating AI-driven credit risk solutions can significantly enhance business performance.

Conclusion

AI is transforming the way NBFCs predict loan defaults by enabling smarter, faster, and more accurate risk assessment. Combined with proper compliance and expert guidance from an NBFC registration consultant, NBFCs can build resilient financial institutions ready for the future.

For businesses seeking NBFC Registration online in India and aiming to operate under a valid NBFC license from RBI in India, embracing AI-powered technologies is a vital step toward long-term success.

The foreign exchange ecosystem in India is evolving rapidly, and Full Fledged Money Changers (FFMCs) are under increasing regulatory and operational pressure. With strict RBI norms governing the full fledged Money Changer license, businesses must ensure transparency, compliance, and robust risk management. This is where Artificial Intelligence (AI) and Data Analytics are transforming the FFMC industry.

The Growing Compliance Challenge for FFMCs

Entities holding an FFMC License in India must comply with multiple regulations, including KYC, AML, FEMA, and RBI reporting requirements. Manual compliance processes often lead to delays, human errors, and higher operational costs. As full fledged Money Changers scale their operations, the complexity of monitoring transactions and identifying risks increases significantly.

How AI Enhances Compliance Monitoring

AI-powered systems can automate and strengthen compliance frameworks for FFMCs. Advanced algorithms analyze large volumes of transaction data in real time to detect anomalies, suspicious patterns, and non-compliant activities.

Generate accurate compliance reports for regulators

This significantly reduces manual intervention and improves regulatory confidence.

Data Analytics for Smarter Risk Management

Data analytics enables FFMCs to move from reactive to proactive risk management. By leveraging historical data, analytics platforms can predict potential compliance risks, customer behavior trends, and exposure to foreign exchange volatility.

This data-driven approach supports sustainable growth while maintaining compliance.

AI in Fraud Detection and AML Controls

AI models are highly effective in identifying complex fraud patterns that traditional systems may miss. For FFMCs, this means stronger AML controls and faster detection of suspicious activities, ensuring adherence to RBI guidelines.

By integrating AI with digital platforms offering FFMCs license online application and management services, businesses can also streamline internal audits and compliance reviews.

Future of FFMC Operations in India

As regulatory scrutiny intensifies, AI and data analytics will become essential tools rather than optional upgrades. FFMCs that invest in intelligent compliance systems will not only safeguard their full fledged Money Changer license but also gain a competitive edge through efficiency, accuracy, and trust.

Conclusion

AI and data analytics are redefining how full fledged Money Changers operate in India. From smarter compliance monitoring to advanced risk management, these technologies empower FFMCs to stay compliant, reduce operational risks, and scale confidently. For businesses seeking long-term success under an FFMC License in India, embracing digital intelligence is the way forward.

In recent years, the Indian financial sector has witnessed a paradigm shift where profitability is no longer the sole measure of success. Social impact investing—investments that generate measurable social and environmental benefits alongside financial returns—is gaining strong momentum. At the forefront of this transformation are Non-Banking Financial Companies (NBFCs), which play a vital role in financial inclusion and sustainable development.

With a supportive regulatory framework and growing investor awareness, NBFCs are uniquely positioned to align profit with purpose. This blog explores how NBFCs can leverage social impact investing while navigating NBFC Registration in India and RBI compliance effectively.

Understanding Social Impact Investing in the NBFC Ecosyste

Social impact investing focuses on funding initiatives that address critical challenges such as:

Financial inclusion

Affordable housing

MSME development

Renewable energy

Healthcare and education financing

NBFCs, due to their flexibility and outreach, are natural vehicles for impact-driven lending and investment. Holding a valid NBFC License in India enables companies to design customized financial products targeted at underserved communities.

Why NBFCs Are Ideal for Social Impact Investing

1. Strong Reach in Underserved Markets

NBFCs often operate in areas where traditional banks have limited presence. Through proper NBFC registration online, companies can scale operations to support rural borrowers, startups, women entrepreneurs, and small businesses.

2. Regulatory Support from RBI

The NBFC license from RBI in India provides a structured framework that balances innovation with financial stability. RBI guidelines encourage responsible lending, transparency, and long-term sustainability—key pillars of social impact investing.

3. Flexible Business Models

Unlike banks, NBFCs can tailor credit products to suit impact-focused sectors. Whether financing electric vehicles or affordable housing, NBFCs can innovate once they complete Online NBFC Registration in India.

Role of NBFC Registration in Building Investor Confidence

Investors in social impact funds seek regulatory clarity and risk mitigation. A properly structured NBFC Registration in India demonstrates:

Legal credibility

Governance transparency

Compliance with RBI norms

Many startups opt for NBFC license online processes to streamline approvals and reduce time-to-market while maintaining compliance.

Digital Transformation and Impact Measurement

Technology is playing a crucial role in aligning profit with purpose. Through NBFC registration online and digital lending platforms, companies can:

Track borrower outcomes

Measure social impact metrics

Improve loan monitoring and recovery

This data-driven approach increases accountability and attracts ESG-focused investors.

Importance of Professional NBFC Registration Consultants

The regulatory process for obtaining an NBFC License in India is complex and documentation-intensive. Engaging an experienced NBFC registration consultant or NBFC Registration Consultant in India helps ensure:

Accurate RBI filings

Faster approvals

Proper capital structuring

Long-term compliance readiness

Professional guidance allows NBFC founders to focus on impact-driven strategies rather than regulatory hurdles.

Popular Social Impact Sectors for NBFCs

NBFCs operating under a valid NBFC license from RBI in India are actively investing in:

Microfinance and financial inclusion

Green and sustainable finance

Affordable healthcare loans

Skill development financing

Agri-finance and rural credit

These sectors offer stable returns while delivering measurable social benefits.

Challenges and Risk Management

While impact investing offers long-term value, NBFCs must address:

Credit risk in underserved segments

Regulatory compliance obligations

Impact measurement frameworks

Proper structuring during NBFC Registration online in India and continuous compliance monitoring help mitigate these challenges effectively.

Conclusion

NBFCs are redefining the future of finance by proving that profitability and social responsibility can coexist. Through structured NBFC Registration in India, strong governance, and impact-focused lending, NBFCs can attract socially conscious investors while delivering sustainable financial returns.

For entrepreneurs and institutions aiming to create meaningful change, obtaining an NBFC License in India is not just a regulatory milestone—it is a gateway to aligning business success with societal progress.

Transparency and trust are critical pillars of the lending ecosystem. As India’s financial sector rapidly embraces digital transformation, Non-Banking Financial Companies (NBFCs) are increasingly exploring advanced technologies to improve efficiency, compliance, and customer confidence. One such transformative technology is blockchain.

This blog explains how NBFCs can leverage blockchain to enable transparent lending while remaining compliant with regulatory requirements such as NBFC Registration in India and RBI licensing norms.

Understanding Blockchain in the NBFC Lending Ecosystem

Blockchain is a decentralized, tamper-proof digital ledger that records transactions in a transparent and immutable manner. For NBFCs, this means enhanced data integrity, real-time verification, and reduced dependency on intermediaries.

NBFCs operating with a valid NBFC License in India can use blockchain to improve loan processing, documentation, repayment tracking, and regulatory reporting.

Why Transparency Is a Challenge for NBFC Lending

Despite regulatory oversight, NBFCs often face challenges such as:

Limited visibility into borrower credit history

Manual documentation and reconciliation errors

Delays in loan disbursement and repayments

Compliance risks under RBI and FEMA regulations

Blockchain addresses these pain points by creating a single source of truth accessible to authorized stakeholders.

Key Use Cases of Blockchain for NBFCs

1. Secure Digital Loan Records

Blockchain enables NBFCs to store loan agreements, borrower data, and repayment schedules on a secure ledger. Once recorded, data cannot be altered, ensuring complete transparency for auditors and regulators.

Smart contracts are self-executing agreements coded on blockchain. These contracts automatically trigger loan disbursements, EMI collections, or penalties once predefined conditions are met.

For NBFCs with an NBFC license from RBI in India, smart contracts help:

Reduce operational costs

Eliminate manual intervention

Ensure compliance with lending terms

3. Improved Credit Assessment and Fraud Prevention

Blockchain allows NBFCs to access verified borrower data across institutions, reducing identity fraud and credit manipulation. This enhances due diligence and supports responsible lending practices.

All repayments recorded on blockchain are time-stamped and immutable. Borrowers and lenders can view real-time repayment status, minimizing disputes and improving trust.

Such transparency strengthens the credibility of NBFCs operating under a valid NBFC License in India.

5. Regulatory Compliance and Audit Readiness

Blockchain simplifies compliance by maintaining an auditable trail of every transaction. Regulators and auditors can access verified records instantly, reducing inspection timelines.

Technology adoption does not replace regulatory compliance. NBFCs must still obtain proper authorization through NBFC registration online and comply with RBI capital, governance, and reporting norms.

Holding a valid NBFC license online application approval ensures:

Legal recognition

Higher trust among investors and borrowers

Smooth integration of emerging technologies

Professional support from an NBFC registration consultant helps NBFCs navigate licensing and technology alignment seamlessly.

Challenges and Considerations

While blockchain offers immense potential, NBFCs must consider:

Data privacy and cybersecurity risks

Integration with legacy systems

Regulatory clarity on decentralized finance models

A phased implementation strategy, guided by compliance experts, helps mitigate these challenges.

Future of Blockchain in NBFC Lending

As India’s fintech ecosystem matures, blockchain is expected to play a central role in credit scoring, co-lending models, and cross-border financing. NBFCs that invest early in transparent lending frameworks will gain a strong competitive advantage.

Securing an NBFC license from RBI in India and adopting blockchain-based systems positions NBFCs as trustworthy, future-ready financial institutions.

Conclusion

Blockchain has the potential to revolutionize NBFC lending by enhancing transparency, reducing fraud, and improving regulatory compliance. However, its success depends on a strong legal foundation and proper licensing.

By completing NBFC Registration in India, obtaining the required RBI approvals, and working with a qualified NBFC Registration Consultant in India, NBFCs can confidently leverage blockchain to build a transparent, efficient, and scalable lending ecosystem.

In India’s tightly regulated foreign exchange ecosystem, trust and compliance are the foundation of every successful transaction. For businesses dealing in foreign currency exchange, credibility is not optional—it is essential. This is where obtaining a Full Fledged Money Changer license plays a decisive role. An FFMC License in India, issued by the Reserve Bank of India (RBI), does much more than grant legal permission to operate; it significantly enhances a company’s reputation with banks, financial institutions, and strategic partners.

This blog explores how full fledged Money Changers benefit from licensing and why FFMC approval is a powerful credibility booster in today’s competitive financial landscape.

Understanding FFMC Licensing in India

A full fledge money changer license in India allows eligible entities to undertake foreign exchange transactions such as buying and selling foreign currency, traveler’s cheques, and prepaid forex cards. Governed under FEMA and regulated by the RBI, FFMCs are expected to meet strict norms related to capital adequacy, compliance, KYC, AML, and reporting.

The FFMC License in India serves as official recognition that a business meets RBI’s regulatory and financial standards, making it a trusted participant in the forex market.

Why Credibility Matters in the Forex Business

Foreign exchange transactions involve high-value funds, cross-border movement of money, and exposure to compliance risks. Banks and partners are cautious about whom they work with, as any regulatory lapse can have serious legal and reputational consequences.

Banks prefer working with entities that are directly regulated by the RBI. An FFMC license demonstrates that your business has undergone detailed scrutiny, including background checks, financial assessment, and operational review. This RBI endorsement reassures banks that the entity is compliant, transparent, and low-risk.

Banks are legally obligated to ensure that their clients comply with FEMA and RBI norms. When a business holds an FFMC License in India, banks can confidently extend services such as:

Nostro/Vostro arrangements

Cash management services

Foreign currency accounts

Payment gateway integrations

Unlicensed or informally operating entities often face repeated rejections or account freezes due to compliance concerns.

3. Reduced Due Diligence Burden

Licensed FFMCs already meet RBI’s KYC and AML requirements. This reduces the additional due diligence banks need to conduct, speeding up onboarding and strengthening long-term relationships. In contrast, non-licensed entities are subject to ongoing scrutiny, audits, and restrictions.

Strengthening Partnerships Through FFMC Licensing

1. Increased Confidence Among Business Partners

Strategic partners—such as travel companies, fintech platforms, exporters, and remittance service providers—prefer to collaborate with entities holding a valid FFMCs lincese in India. Licensing assures them that the business operates within legal boundaries and follows standardized procedures.

This credibility opens doors to:

White-label forex partnerships

Franchise and sub-agent models

Cross-border payment collaborations

2. Competitive Advantage in the Market

In a crowded forex market, having an RBI-approved FFMC license differentiates your business. Partners are more likely to choose licensed full fledged Money Changers over unregulated competitors because the risk of regulatory non-compliance is significantly lower.

This advantage often translates into higher transaction volumes and stronger commercial terms.

3. Long-Term Business Sustainability

Partnerships thrive on stability. An FFMC license signals that the business is built for long-term operations, not short-term gains. This assurance encourages partners to invest time, resources, and technology into collaborative growth.

Role of Online FFMC Licensing in Building Credibility

With regulatory processes becoming more digitized, businesses can now apply for FFMCs license online through professional consultants. Online licensing ensures:

Faster documentation and submission

Better compliance tracking

Reduced procedural errors

Opting for FFMCs license online not only simplifies the application process but also reflects a business’s commitment to transparency and modern governance—qualities highly valued by banks and partners alike.

Compliance as a Continuous Credibility Factor

Obtaining the license is only the beginning. RBI expects FFMCs to maintain ongoing compliance through:

Periodic reporting

Regular audits

Adherence to updated KYC and AML norms

Businesses that remain compliant retain their credibility and avoid penalties, suspension, or cancellation of their FFMC License in India.

Conclusion